This week’s European energy dealflow ticks up across wind, battery-storage, hydrogen and solar. With capital costs still elevated, platform M&A stands out in offshore wind.

See all the deals and analysis, including:

- BESS remained active (7 deals), reinforcing the sector’s strategic consolidation seen over the past two months. The sale of a 50% stake in a 500 MW project by CIP to AIP Management signalled market maturity, with strong contracted revenues underpinned by a 15-year Capacity Market agreement.

- Hydrogen advances through partnerships and pilots: Nordic hub in Åland, German corridor, modular electrolysers in Poland, and UK ammonia cracking.

- Institutional capital expands platforms: Aviva/Astatine launch €800m vehicle; European Energy recycles capital via solar-storage stake sale in Latvia.

Want to talk about any of these insights? Connect with me on LinkedIn.

Cocktails & networking on UK Energy M&A

Cocktails, insights and connection awaits dealmakers on November 20.

Join Ideals VDR and fellow energy dealmakers for an exclusive networking evening at Black Lacquer, Hyde London City.

Deals breakdown

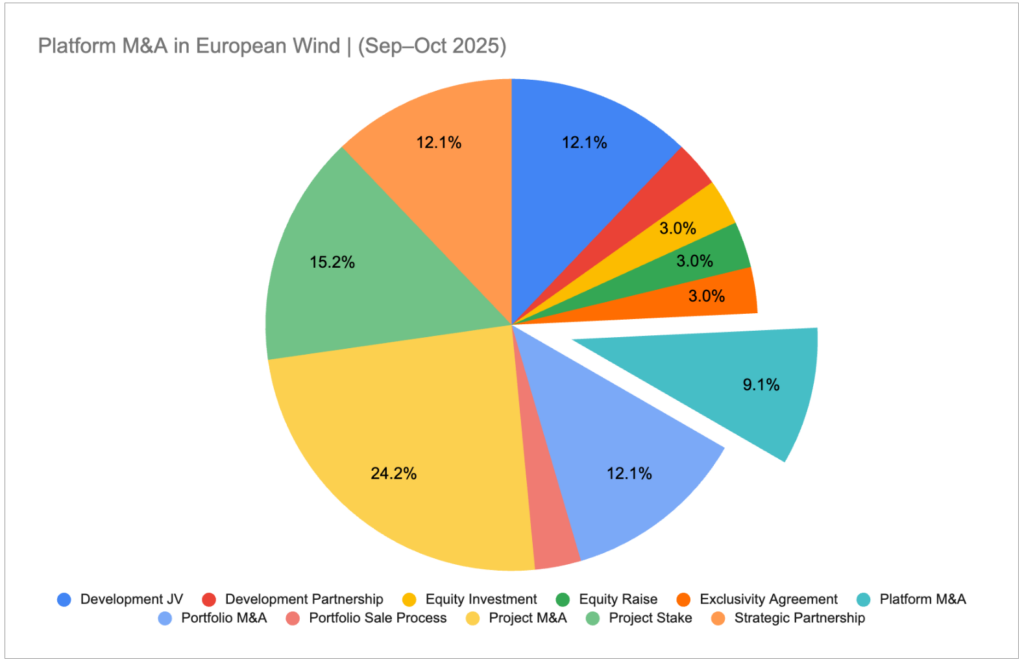

Offshore wind: is European M&A becoming a case study in adaptability?

2025 has been marked by fragmentation and growing complexity in geopolitical and trade relations. And today, in the wake of the Ocean Winds–Allianz deal, we look at a strategy that, based on our curation, appears to be the choice of many offshore wind dealmakers: platform M&A.

A few economic factors help explain why:

- The cost of capital (WACC) is higher, with European rates still above the 2021–22 average. This feeds into a systemic effect that, according to Ember, has already lifted turbine costs by 10% in 2024.

- Recent years have also piled cost pressures onto the sector: project costs are up 30–40% since 2021, per BCG. Input inflation and interest rates are doing the heavy lifting here.

Is platform M&A going to become a trend in offshore wind M&A?

Between September and October, positioning around platform M&A, investing in anchor companies with teams and cash flows already in place, emerged as an alternative for dealmakers seeking to avoid concentrated asset risk, such as buying a single park.

Although platform M&A accounted for only 9.1% of wind announcements over the past two months (less frequent than project acquisitions or portfolio rotations), its strategic weight was meaningful.

- Moves like the one by Ocean Winds (the EDP–Engie JV) this week suggest that, with higher WACC and volatile capex, many buyers see strong strategic value in backing established teams, processes and pipelines.

- That approach captures synergies and optionality for bolt-ons rather than concentrating risk in a single park.

Could this share reach double digits?

The opportunities are there, but it depends on the ability to capture value such as:

- Accelerating your deal machine, shortening the time from origination to build, partial sell-down and reinvestment.

- Reducing risk by mixing stages (from greenfield to operational) and lowering WACC via the anchor company’s know-how and relationships.

- And, of course, the synergies already mentioned.

It’s worth considering the strategy before you’re back on negotiation tables.