Daniel Black

Daniel Black

Hello,

The Chancellor gave her spring statement this week amid news that market turmoil and US tariffs had caused the OBR to halve its growth forecast for the UK economy from 2% to 1% for 2025. But on the bright side, it has upgraded its growth forecast for next year and every year thereafter.

We also have data in our Market Trends section which shows that the weakening dollar is opening up deal opportunities for European investors.

In other news this week:

- Regulatory delays killed Carlyle’s Energean deal

- AstraZeneca is splashing $2.5bn on a Chinese R&D hub

- Ardonagh is close to securing $2.5bn to fund more M&A

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Trump tariffs loom over Britain’s debt-laden economy

- UK in talks over US car tariffs, could look at Tesla subsidies, finance minister says

- The Office for Budget Responsibility (OBR) forecasts UK inflation to average 3.2% in 2025

- UK’s 2025 growth forecast halved to 1.0%, OBR says

- BP weighs stake sales in two Gulf of Mexico projects

- BP looks to sell petrol station chain in Austria, as slims downstream

- Wood Group poised to extend takeover talks with UAE’s Sidara

- Thames Water had feared it might be left with just £39m cash by month-end

- NIOX supports sweetened takeover bid from Keensight

- Repsol and NEO Energy agree to merge their UK North Sea oil and gas businesses to create a joint venture

- AstraZeneca investing $2.5 billion in China as drugmaker seeks to recover from scandals

- BAE is ready to boost £1bn investments amid defense boom

- UK food group Greencore increases bid for rival Bakkavor

- Carlyle and Energean mutually end $945m transaction following regulatory delays

- James Hardie is set to buy building products group Azek for nearly $9bn

- VivoPower skyrockets on $120m takeover offer by Energi Holdings

- Ardonagh ‘close to securing up to $2.5bn from investors’

- Bridgepoint-backed Burger King UK seeks refinancing to fund growth

- Plus500 is to acquire Mehta Equities

- Drax beats Foresight in bid to buy Harmony Energy Income Trust

- Tullow Oil is to sell its Gabon assets for $300 million

- Kondor AI to create AI agent-focused firm with acquisition of Ora Tech

- Kenmare Resources profits plunge on lower prices, but firm receives a non-binding takeover proposal from a consortium including Oryx Global Partners Ltd and former Managing Director Michael Carvill

- London & Capital rebrands into W1M after Waverton merger

- HgCapital Trust invests £124m software firm IFS

- Renewi shareholders approve takeover by Macquarie at meetings

- Ithaca Energy PLC struck a USDm 193 deal to acquire Japex UK

- E&P Ltd, boosts its stake in the Seagull oil field to 50%

- Warehouse REIT gauges “final” £489m Blackstone tilt

- MEAG is selling 157 MW of British wind and solar parks to Engie

- LondonMetric to acquire Highcroft Investments in £43.8m deal

- AJ Bell sells non-platform Platinum pensions business to InvestAcc for up to £25m

- CLS is to sell “very successful” student development for £101m

- Montagu Private Equity mulls offer for Advanced Medical Solutions

Salaries and bonuses

- HSBC bonus payouts spark exodus fears, with junior bankers leading the charge ahead of expected Q2 job cuts

- Panmure Liberum pays zero bonuses for third year running

Job moves

- HSBC fired investment bankers on bonus day and gave them no bonuses

- Private equity bought up UK wealth. Now it needs CEOs

- UK’s Sage Group says Cartin to replace Howell as CFO next year

- Rathbones’ CEO Paul Stockton to retire

- Goldman ramps up EMEA wealth hires, Rathbones’ new chief

- Goldman Sachs plots wealth hiring spree in UK, Switzerland and Middle East

- Linklaters promotes 34 new partners

- DWS appoints Global Head of Private Credit amid alts reshuffle

- Monzo promotes long-term employee Andy Smart to chief product officer

- Pemberton appoints Senior Advisor for Nordic region

- HSBC tech staff may be first to lose their jobs to Citadel Securities. Goldman Sachs’ 26% London pay rise

- Teachers Building Society names Gavin Opperman as new CEO

- Banking veteran Guy Noble named as new UK CEO of Guavapay

- CVC appoints Jean-Pierre Saad as a new Managing Partner

- London BNP MD moves to Paris for SocGen privates team

- Morgan Stanley’s cuts include this senior credit trader in London

Market trends

European buyers eye US deals amid currency shifts

A stronger euro and a weaker dollar are making US acquisitions increasingly attractive for European buyers, according to a report in Mergermarket. Ongoing uncertainty over US trade has weighed on the dollar, while the end of Germany’s “debt brake” has bolstered the euro.

The author highlights that deal value had already increased 46% in 2024 compared to 2023, even before the recent moves in the forex market. The US now captures 72% of Europe’s outbound transactions.

Notable deals include UK-based Celnor Group’s purchase of John Turner Consulting and Amcor’s all-stock acquisition of Berry Global Group.

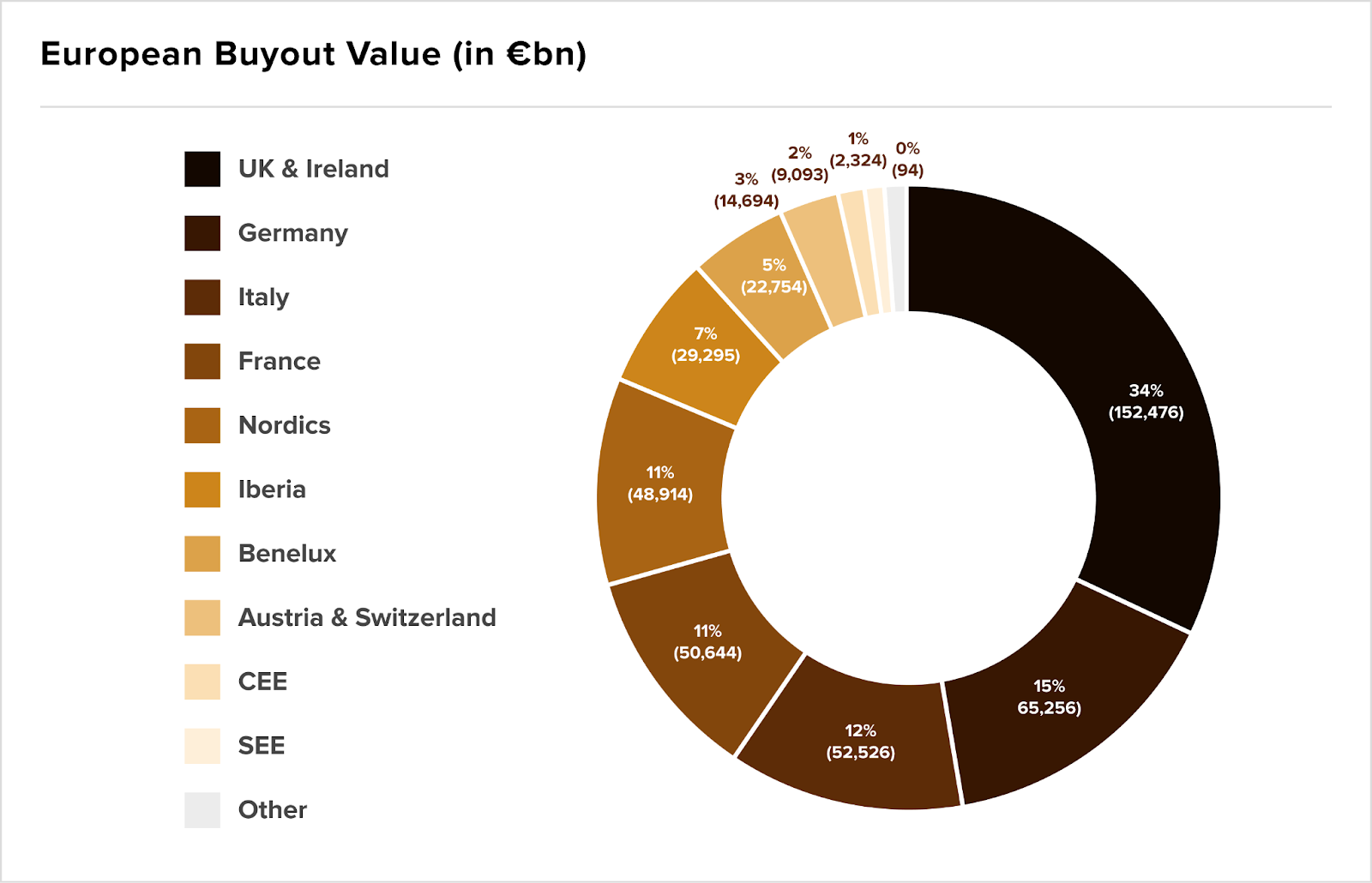

European PE regains strength

After several years of decline following the market boom in 2021, European PE saw a slight uptick in 2024. Deal volumes remained relatively steady rising 3.3% to 3,975 transactions, while total deal value climbed 23% to £285bn – well above pre-pandemic levels.

Falling inflation and interest rate cuts from the ECB and BoE helped restore confidence, driving a shift towards larger deals. The average deal value went up from £60m to £71.7m, with megadeals (>€1bn) up 77% YoY.

According to PwC’s PE Trend Report 2025 , the UK and Ireland retained their position as Europe’s largest buyout market, accounting for 34% of total PE deal value in 2024. A wave of LSE delistings, including the £4.2bn take-private of Darktrace and the £5.3bn delisting of Hargreaves Lansdown, opened doors for PE firms.

Separate data shows that PE buyouts in the UK rose for the third consecutive quarter in Q4 2024, from 411 in Q3 to 433 in Q4. This helped push the UK’s annual transaction volume to 1,571, up from 1,391 in 2023.

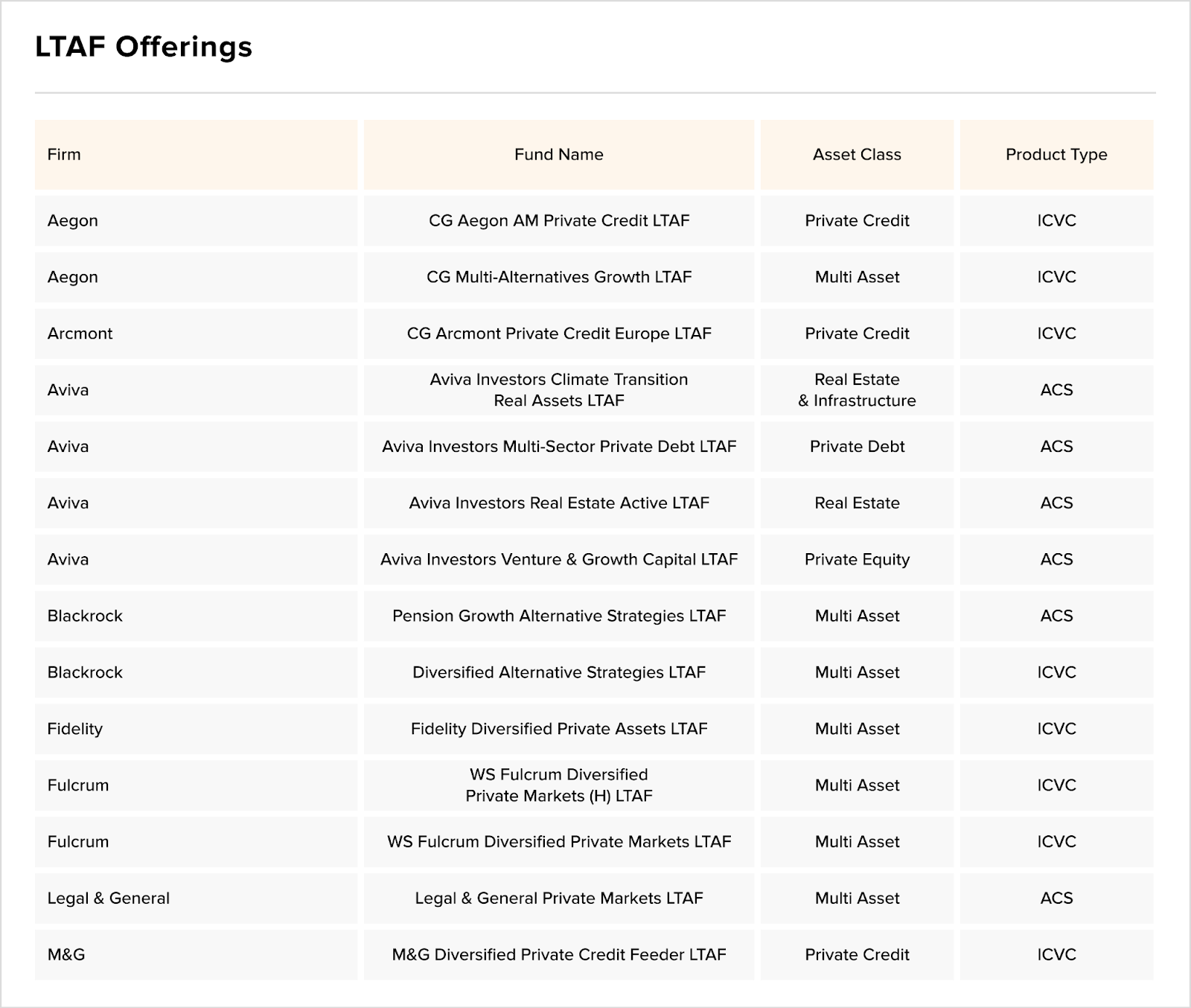

Private markets gain traction

And finally, MorningStar has an interesting report on the continuing growth of the UK’s private investment market. Long-term asset funds (LTAFs) are gaining momentum, with the FCA’s registry now listing 23 approved sub-funds.

Schroders Capital leads the charge, with six approved LTAFs. Other major asset managers like Aegon, Aviva, BlackRock, Fidelity, Legal & General, and Willis Towers Watson are leveraging the structure to increase exposure to unlisted assets.

The ever increasing role of LTAFs in wealth and pension markets signals a shift in private market accessibility, potentially driving more deals in alternative assets and PE.

Fundraising

IPOs

- Air Baltic says Ukraine ceasefire would help IPO prospects

- UK billionaire Michael Spencer warns of ‘slow corrosion’ in London IPOs